|

|

ch verstehe nicht, warum man sagt, dass die Verjährungsfrist 6 Jahre beträgt. Nun, ich habe die Prospekte von 8 Anleihen gelesen, in denen die darin festgelegten Bedingungen unterschiedlich sind, und zwar wie folgt: 1. Republik Venezuela, ISIN: USP 17625AA59, Laufzeit: 05.07.2023, Verschreibung: Kapitalwert: 10 Jahre und Zinsen: 3 Jahre. 2. Republik Venezuela, ISIN: USP97475AP55, Fälligkeit: 13.10.2024, Verschreibung: Kapitalwert: 10 Jahre und Zinsen: 3 Jahre. 3. Republik Venezuela, ISIN: XS0217249126, Ablaufdatum: 21.04.2025. Kapitalwert: 10 Jahre und Zinsen: 3 Jahre. 4. Republik Venezuela. ISIN: US922646AS37. Ablauf: 15.09.2027. Rezept: Im entsprechenden Beipackzettel habe ich nichts zum Rezept gefunden. 5. Republik Venezuela. ISIN: USP97475AJ95. Ablauf: 31.03.2038. Verschreibung: Kapitalwert: 10 Jahre und Zinsen: 3 Jahre. 6. PDVSA. ISIN: USP7807HAT25. Ablauf: 16.05.2024. Verschreibung: Hauptwert und Interesse: 6 Jahre. 7. PDVSA. ISIN: XS0294364954. Ablauf: 12.04.2027. Kapitalwert und Zinsen: 6 Jahre. 8. ELECAR/CORPOELEC. ISIN: XS0356521160. Ablauf: 10.04.2018. In der Packungsbeilage habe ich nichts zum Rezept gefunden. Fazit: Wann kommt es eigentlich zu Verschreibungen? ?Die in den Prospekten festgelegten Zeiträume oder die kommentierten 6 Jahre? ?Und weil? Gibt es in den Gesetzen des Staates New York eine übergeordnete Bedingung für gleiche oder nicht gleiche Situationen? Ich lade alle ein, sich zu diesem Thema zu äußern, wofür ich Ihnen im Voraus danke.

By Juan Pablo Álvarez

Argentina and Ecuador restructured their debts with private creditors in 2020 within the framework of the coronavirus quarantines.

They did it in a very different way.

While Guillermo Lasso’s administration took three months and did it after a previous agreement with the International Monetary Fund, Alberto Fernández’s team took more than twice as long and without a previous deal with the IMF.

This difference caused both restructurings to have divergent paths: as an example, while Argentina closed 2022 with a country risk of 2,162 units, Ecuador did the same at 1,255 basis points.

However, the political crisis faced by President Lasso in Ecuador – he has just dissolved the Assembly and called for elections for executive and legislative positions, anticipating his impeachment – severely damaged sovereign bonds and, at this moment, Ecuador’s country risk stands at 1,857 points (against 2,596 of Argentina).

Both states currently have the second and third worst country risk in Latin America since the first place is occupied by Nicolás Maduro’s Venezuela (35,587.91 units).

In this context, the Argentine consulting firm Quantum Finanzas prepared a study on the evolution of both debt restructurings.

THIS IS HOW ARGENTINA’S AND ECUADOR’S DEBTS EVOLVED

The average price of Ecuador’s sovereign debt in dollars is 40/100, while Argentina’s is 26.5/100 (Global bonds).

“The recent sharp correction in the price of Ecuador’s (from almost 60/100 in January) can, in part, be associated with general asset price movements in the region following last year’s Q4 rally, but also with political tensions,” the Quantum paper notes.

According to Quantum, the upside of Argentina’s debt prices in a scenario of relative normalization is higher -even considering a future restructuring, entry prices would more than offset it- than that of Ecuadorian bonds”.

DIFFERENCES BETWEEN THE TWO COUNTRIES

The Quantum report notes that Ecuador’s economy is “stable” and has been dollarized since 2000.

It also notes that the country has maintained positive growth rates in recent years, but the political crisis has escalated.

“The outcome of the political crisis anticipates greater strength and dominance of the line of former President Rafael Correa.”

“In Argentina, on the other hand, the economic crisis has been manifesting itself in one form or another for some time and was practically constant in the period we are considering.”

“This derives in political tensions, which, however, are contained within a general institutional framework that maintains republican forms and practices, without interruptions,” Quantum compares.

Quantum Finanzas maintains that Ecuador’s economic indicators are “substantially better” than those of Argentina in terms of inflation, external sector, fiscal balance, and public debt, although it clarifies:

“The question is whether dollarization and its rigidity in terms of economic policy decisions, beyond the fact that it allowed sustaining stability for many years in Ecuador and that, in general, the economy shows better indicators than Argentina, is more advantageous to achieve a sustained growth that allows reducing the costs of indebtedness”.

This doubt raised by Quantum Finanzas is because the Ecuadorian economy is dollarized and is usually the model used as an example by those who want to dollarize in Argentina.

“Both countries face political difficulties that impact their economies (crack). In Ecuador, even with a history of tensions and greater fragility”, summarizes the report.

With information from Bloomberg

News Latin America, English news Latin America, Argentine econo

CARACAS, May 15 (Reuters) - Venezeula's political opposition - recognized by the U.S. as the country's legitimate government - was asked by a key creditor group on Monday to back the suspension of a statute of limitations on repayments for defaulted government bonds.

President Nicolas Maduro's government in March proposed a five-year suspension through 2028 or until the United States lifts sanctions that impede a debt restructuring.

A deadline on some bonds is set to expire in October, six years after the Venezuelan government stopped paying down the debt, meaning those bond holders could lose their right to ask courts to order repayment.

The Venezuela Creditors Committee (VCC) which holds billions of dollars in defaulted Venezuelan bonds said in a statement it wanted the opposition to lend its support to the proposal.

The opposition has yet to take a stance on the issue.

"Without such an agreement... significant risks remain," the statement said, noting the potential for additional litigation that could disrupt trade and other efforts to boost Venezuela's ailing economy.

The opposition-controlled national assembly this month received a license from the U.S. Department of the Treasury to carry out debt settlement deals with the Maduro government and state oil company PDVSA.

Venezuela and PDVSA owe more than $60 billion in bonds that they stopped payment on in late 2017, triggering the default. The VCC represents creditholders for some $10 billion of that debt.

The bonds were issued under New York state law and include a statute of limitations clause stating that the interest payments due to bondholders is not legally enforceable after six years of non-payment.

Our Standards: The Thomson Reuters Trust Principles.

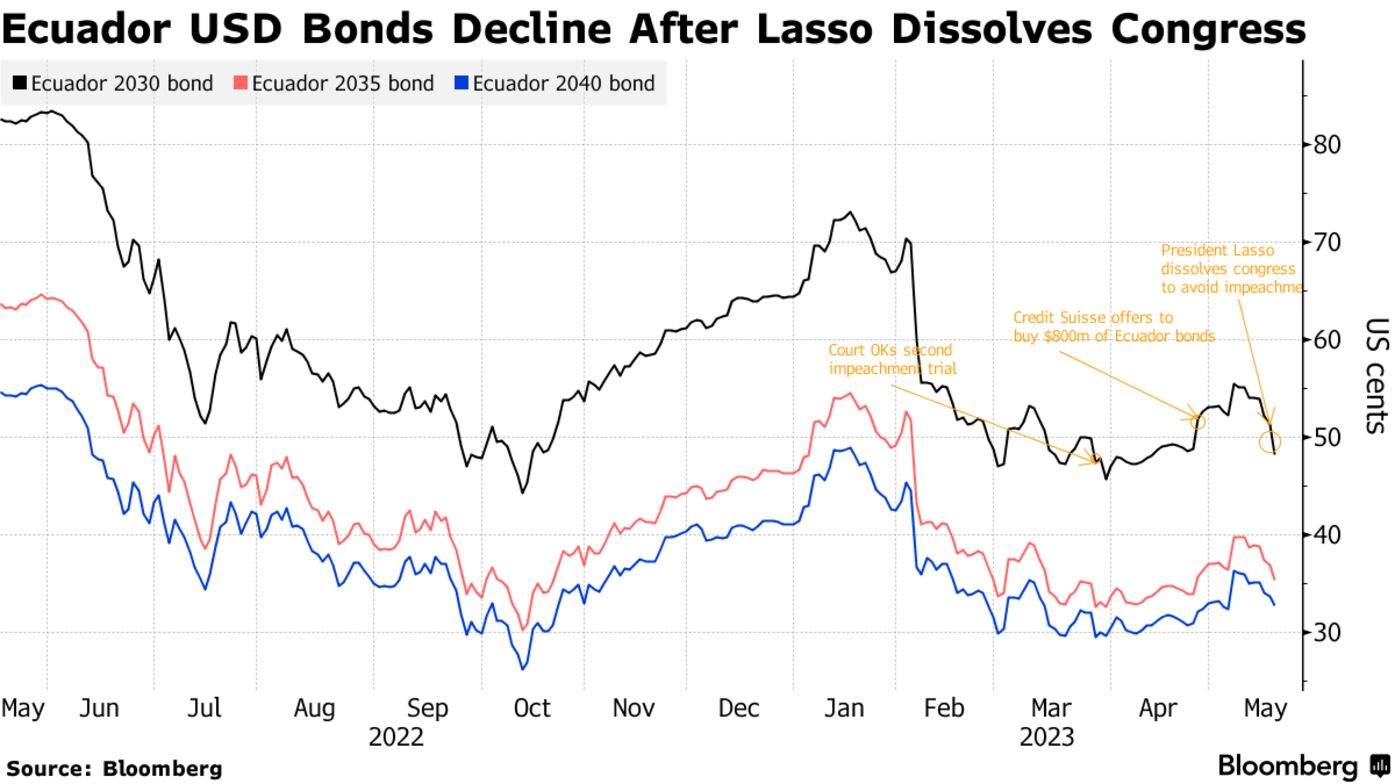

Ecuador’s bonds have handed investors losses of 19% this year, the third-worst in the developing world, according to an index of peers. The selloff began in February, when traders took Lasso’s defeat in a constitutional referendum as a sign of his weakening mandate. Since then, the opposition-led National Assembly has started a second impeachment bid for the former banker, who took office nearly two years ago.

Ecuador bonds sank on Wednesday after President Guillermo Lasso opted to dissolve congress and call for early elections in a bid to avoid impeachment.

Debt from the South American nation posted some of the biggest declines in emerging markets, with bonds due in 2030 sliding as much as 5.3 cents to about 46 cents on the dollar, the lowest in more than a month, according to indicative pricing data collected by Bloomberg. The extra yield investors demand to hold Ecuador’s debt jumped more than 80 basis points to 1,860, according to JPMorgan Chase & Co. data.

Ecuador’s bonds have handed investors losses of 19% this year, the third-worst in the developing world, according to an index of peers. The selloff began in February, when traders took Lasso’s defeat in a constitutional referendum as a sign of his weakening mandate. Since then, the opposition-led National Assembly has started a second impeachment bid for the former banker, who took office nearly two years ago.

Read more: Ecuador’s President, Facing Impeachment, Forces New Elections

The snap election opens the door for the comeback of a left-leaning leader in a nation that has defaulted 11 times on its overseas bonds since its independence in 1830.

Allies of former President Rafael Correa won key local races in a February vote held the same day as Lasso’s failed constitutional referendum. The results marked a comeback in support for Correa, who stung markets in 2008 by defaulting on most of Ecuador’s overseas debt and labeling bondholders as “true monsters.” Facing an eight-year jail sentence for graft, he’s barred from running for office himself, and has been granted asylum in Belgium.

Here’s what investors and economists are saying:

Barclays economist Alejandro Arreaza

Citigroup strategists led by Dirk Willer

Katrina Butt, a senior economist at AllianceBernstein in New York

Sergio Armella, Goldman Sachs economist in New York

| MLIV PULSE SURVEY |

|---|

| Are you bullish or bearish on emerging markets? Share your views here. |

Oren Barack, managing director of fixed income at New York-based Alliance Global Partners

Siobhan Morden, managing director for Latin America fixed income at Santander in New York:

Ramiro Blazquez, head of strategy at BancTrust & Co. in Buenos Aires

Senegal Makes $471 Million Payments to Service Foreign Bonds Dakar, Senegal. Photographer: Damian Lemański/Bloomberg By Ray Ndlovu and ...